Просмотр новости

Найдите то, что Вас интересует

Спутники

Спутники РН

РН SpaceX

SpaceX Роскосмос

Роскосмос NASA

NASA

Monetary Council makes a move, but what will it entail?

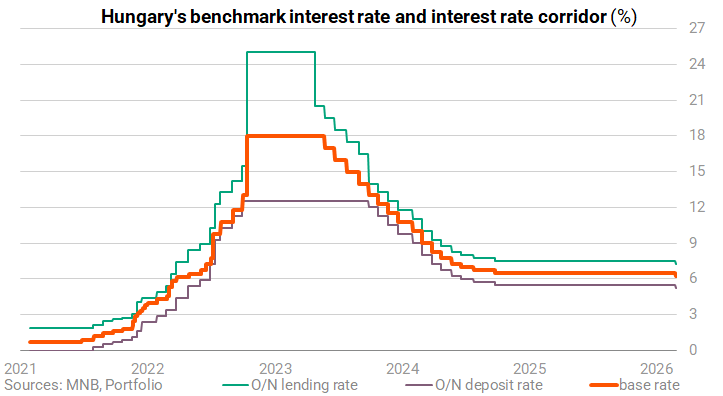

In line with expectations, the Monetary Council of the National Bank of Hungary (MNB) lowered the base rate by 25 basis points to 6.25% on Tuesday. This marked the first change to the benchmark rate since September 2024. This was widely anticipated, as the market had been anticipating an interest rate cut since December, particularly after inflation came in lower than expected at 2.1% yr/yr in January. At a press conference following the decision, central bank Governor Mihály Varga emphasised that financial market stability and the improving inflation trajectory had both played a key role in the decision to cut interest rates.

In light of January's data, the inflation picture looks increasingly favourable, as monthly price increases this year have been very modest (0.3%), compared to the strong (1.5%) monthly repricing seen at the beginning of last year. Therefore, the 2.1% inflation figure reported a few weeks ago could fall further in February, potentially dropping below 2%, if restrained repricing behaviour continues into the spring.

Although there are still serious uncertainties, the annual rate of inflation is within the central bank's target range, even with the previously estimated 1-1.5 percentage point impact of margin caps.

Added to this is the stable exchange rate of the forint in recent weeks, with the Hungarian currency remaining unaffected by geopolitical tensions and strengthening to below 380 against the euro. This is a key factor for the MNB, which has repeatedly emphasised that a stable and strong exchange rate is crucial for keeping inflation down.

In other words,

all the conditions were now in place for the central bank to start reducing interest rates.

Changes in the base rate can affect almost every area of our lives because the purpose of the monetary transmission mechanism is to ensure that money market rates align with this benchmark rate. In other words, lower central bank interest rates can lead to lower interest rates on loans and bank deposits. However, it is true that many products on the credit and savings markets, such as SME or mortgage loans and retail government securities, do not follow movements in the base rate.

Therefore, monetary transmission through the credit channel is currently weak in Hungary, meaning that changes in the base rate have only an indirect and minor impact on most segments of the credit market. On the one hand, according to the latest data from the MNB, the proportion of subsidized loans is 81% in housing loans, 35% in SME loans, and 17% in total corporate loans in new placements, and the interest rate on these is typically fixed at 3%.

Conversely, interest rates on market-rate home loans and long-term corporate loans are not linked to the base rate or the closely related rate, which is also currently falling. Instead, they are linked to the yield on 10-year government bonds and the interbank interest rate swap (BIRS) with a similar maturity.

Domestic monetary policy has a much more indirect impact on these longer-term yields, since government bond yields are also affected by fiscal risks, sovereign debt ratings, the geopolitical situation, government expectations linked to extra profit tax breaks, and investors' yield expectations. However, if expectations of further interest rate cuts intensify, this could be reflected in long-term yields in the shorter term.

Only loans tied to BUBOR as a reference rate can be directly affected by a decrease in the base rate. In the retail segment, however, this essentially only applies to Lombard loans. These loans represent a niche market and may become cheaper as a result of this change. Since 2022, the interest rates on BUBOR-linked mortgage loans with a maximum interest period of one year (as well as those with a maximum interest period of five years) have been protected by an interest rate cap, with their reference rate fixed at the October 2021 level of just under 2%.

As things stand, the interest rate cap will not permit changes to BUBOR to be reflected in repayment instalments until June 2026. BUBOR already plays a key role in short-term, forint-based lending to companies, and these loans could become roughly half a percentage point cheaper. For example, the interest rate could be 0.15% for a one-year term and around 0.45% for a three-year term, which would reduce the monthly debt burden for those with annuity-based loans.

As far as bank deposits are concerned, 86% of those held by individuals and 60% of those held by companies are not fixed-term. Current account deposits with interest rates of 0% or close to 0% will not be affected by the reduction in the base rate. The vast majority of publicly available fixed-term deposits (which are not priced individually for large corporations) also have fixed interest rates. Therefore, it is more likely that the lower interest rate environment will lead to a slight decrease in the pricing of newly advertised deposits than in the pricing of existing deposits. Interest rates linked to BUBOR and based on offers to large corporations may decrease in the area of corporate cash management, but these rates are not publicly available.

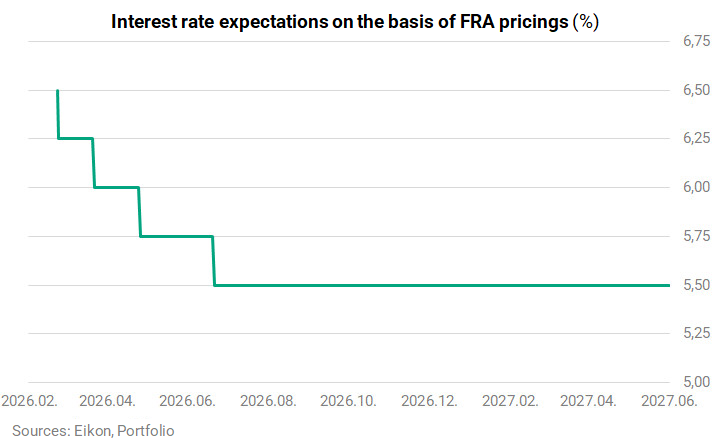

Clearly, the interest rate cut will not be reflected in the terms and conditions of banking products overnight. However, this effect is reinforced by analysts' expectations of a cycle of interest rate cuts, meaning the benchmark rate could be significantly lower in the medium and long term. Although Mihály Varga was cautious in his statements, emphasising that no commitment had been made to a cycle of interest rate cuts, the market expects cuts in March, April and June.

Market pricing currently anticipates a further three 25-basis-point cuts by the end of the year, which would bring the interest rate to 5.5% in December. The graph clearly shows that investors expect the interest rate path to be front-loaded this year, meaning the central bank could be "done with" the entire easing cycle in the first half of the year.

Of course, the future of margin caps may be decided before then, which could have a significant effect on inflation. The same applies to the extent and nature of the corrective measures that the new government will implement in autumn in an attempt to adjust the budget deficit.

Although the market is anticipating further rapid interest rate cuts, not all analysts agree. According to Sándor Jobbágy, chief macroeconomic analyst at Concorde Securities, the central bank governor's press conference on Tuesday suggested that the MNB may wait to take further action in the coming months, even if inflation figures are relatively favourable.

The wait-and-see approach may provide an opportunity to analyse the effects of geopolitical risks, such as oil import problems and intensification of Hungarian-EU disputes, as well as increased volatility of the forint due to the April parliamentary elections. This would allow the MNB to avoid exacerbating these risks with a series of potentially overly rapid interest rate cuts. Jobbágy believes that further interest rate cuts will only be possible in the second half of the year and, even then, only to a limited extent.

Despite the central bank governor emphasising that this cut should not be interpreted as the start of an easing cycle, Péter Virovácz expects another interest rate cut in March. According to the ING Bank analyst, only geopolitical developments or a possible weakening of the forint could torpedo this following the expected favourable February inflation data.

In addition to its direct economic effects, a looser monetary policy also has indirect effects, primarily on financial markets. Lower interest rates from the central bank may also lead to lower yields on government securities, although this would be more noticeable if investors were to associate the Hungarian economy with lower risk in the long term.

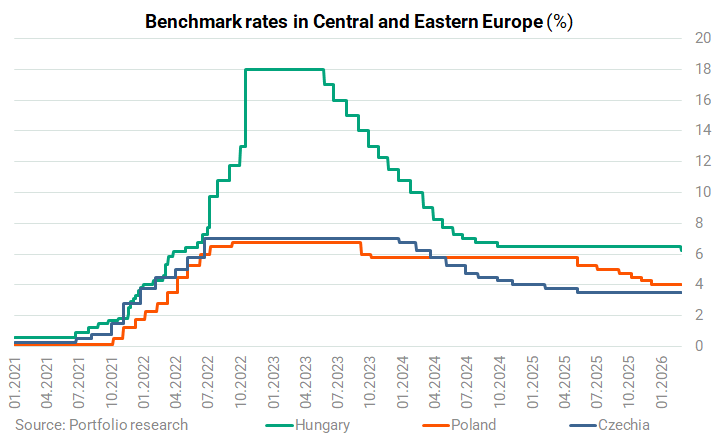

Perhaps even more important is the impact on the forint exchange rate. Over the past year, the relatively high benchmark interest rate of 6.5% has often been cited as one of the most important factors supporting the Hungarian currency. It played a significant role in the currency's strong appreciation in 2025 and the stability observed at the beginning of this year.

Based on this, we can reasonably be concerned about the future of the forint, as its strength may diminish if interest rates fall. However, it is worth noting that the interest rate advantage of the Hungarian currency has grown so much that it is unlikely to be affected by a gradual cut in interest rates. Since January last year, the Polish central bank has lowered interest rates by 175 basis points, while the Czech central bank has cut them by 50 basis points. This means that the relative position of the forint has actually improved so far. However, part of this improvement may be lost, and further interest rate cuts are also on the horizon in other countries in the region.

The market has now priced in the aforementioned 100-basis-point interest rate cut by the end of the year, meaning investors no longer expect interest rates to remain unchanged.

While a temporary fluctuation in the forint exchange rate is conceivable as some market participants close their positions, a sustained weakening trend is unlikely.

According to Péter Virovácz, market players are not concerned about the disappearance of the forint's interest rate advantage. In fact, they are more likely to seek new entry opportunities in the market and open further positions in the Hungarian currency in the coming weeks. However, he believes that,

with the elections approaching, it is difficult to imagine the forint reaching new highs alongside the MNB's interest rate cuts, and that a stable exchange rate is more likely.

The possible outcome of the April elections appears to be of much greater importance to the market than interest rates at present. There is growing speculation that many investors view a potential Tisza Party victory positively and anticipate favourable economic developments. This could strengthen the forint further in the coming weeks, until the election results are known.

Cover photo: Ákos Stiller/Bloomberg via Getty Images

| # | Наименование новости | Тональность | Информативность | Дата публикации |

|---|---|---|---|---|

| 1 | Hungarian central bank lowers interest rates after almost 18 months | 0 | 5 | 24-02-2026 |

| 2 | Hungary cenbank does not commit to rate cut cycle - Governor | 0 | 5 | 24-02-2026 |

| 3 | Hungary central bank releases rationale for rate cut | 0 | 5 | 24-02-2026 |

| 4 | Багаевская: Ночь 18 дек, Вт | 0 | 0 | 17-12-2018 |

| 5 | Спрос на перевозки из Китая и Казахстана в Беларусь вырос в 3 раза | 0 | 0 | 28-01-2025 |

| 6 | ISL | Bengaluru will be keen on regaining consistency as it faces Mohammedan | 0 | 0 | 10-01-2025 |

| 7 | Глава 13 "Подозрения и Обман": Джокер и голубь с большой ... | 0 | 0 | 21-02-2025 |

| 8 | Газинский: сборная России в матче против шведов будет играть только на победу | 0 | 0 | 19-11-2018 |

| 9 | ☝Мамы, хотите действительно отдохнуть и не думать как накормить любимых, ... | 5 | 6 | 29-06-2026 |

| 10 | Яндекс.Маркет рассказал о спросе у москвичей на шины | 0 | 0 | 15-10-2019 |